Chapter 13 bankruptcy representation guided by 80 years of experience in St. Louis and the surrounding area.

If you are struggling with debt in St. Louis and the letters from creditors have started turning into lawsuits, garnishment notices, or foreclosure warnings, Chapter 13 bankruptcy may give you a way to reorganize what you owe. Chapter 13 is not liquidation. It is a repayment plan, approved by a federal court, that runs three to five years and consolidates your obligations into a single monthly payment. Pioletti Pioletti & Nichols has handled bankruptcy matters for over 80 years. Our St. Louis, MO Chapter 13 bankruptcy lawyer can assess whether this filing makes sense for your situation.

Chapter 13 Bankruptcy Lawyer St. Louis, MO

People sometimes refer to Chapter 13 as the wage earner’s plan. The requirement for regular income is central to how Chapter 13 works. To file under this chapter, you need regular income, enough to cover basic living expenses and still fund a monthly payment to your creditors through a court-supervised plan. The debtor proposes how much to pay and over what period. Creditors cannot pursue collection while that plan is in effect.

Chapter 13 cases in St. Louis are filed with the U.S. Bankruptcy Court for the Eastern District of Missouri. The Chapter 13 bankruptcy process starts with the petition and ends with a discharge order after the final plan payment. Whether filing makes sense depends on what the debtor earns, what is owed, and what assets are at stake.

Types of Bankruptcy and Debt Relief Cases We Handle in St. Louis

No two debt situations are identical. Someone facing foreclosure on a home in South City has different priorities than a wage earner in Chesterfield whose paycheck is being garnished. The filing strategy has to match the problem. Pioletti Pioletti & Nichols handles the following bankruptcy and debt relief matters in St. Louis.

- Chapter 7 bankruptcy. This is the liquidation option. Most unsecured debts are eliminated, and the process wraps up in roughly three to four months. It works best when the filer does not have substantial assets to protect and qualifies under the means test.

- Chapter 11 bankruptcy. Designed primarily for businesses, though individuals whose debts exceed the Chapter 13 limits can also file under this chapter. The debtor reorganizes while continuing to operate under court oversight.

- Car repossession. A Chapter 13 filing can stop a repossession before it happens. In some circumstances, it can even force the return of a vehicle seized within a narrow window before the petition was filed. The car loan gets folded into the repayment plan.

- Debt consolidation. Chapter 13 works as court-supervised consolidation. One payment goes to the trustee each month, and the trustee distributes it to creditors according to the confirmed plan.

- Foreclosure. This is one of the primary reasons St. Louis homeowners file Chapter 13. The automatic stay stops the foreclosure immediately, and the plan allows the debtor to catch up on missed mortgage payments over three to five years while continuing to live in the property.

- Wage garnishment. The automatic stay cuts off garnishments the moment the petition is filed. The debt that triggered the garnishment is then handled through the plan rather than through involuntary paycheck deductions.

- Secured debt restructuring. Certain secured debts can be restructured under Chapter 13 when the collateral is worth less than the balance owed. A cramdown reduces the secured portion of the debt to the asset’s current value, and the remainder is treated as unsecured.

- Tax debt repayment. Some tax obligations survive bankruptcy and cannot be discharged. But Chapter 13 lets the debtor repay those taxes through the plan over three to five years, which is often preferable to dealing with the IRS or state collection directly.

Why Choose Pioletti Pioletti & Nichols as My Chapter 13 Bankruptcy Lawyer in St. Louis, MO?

Bankruptcy Representation in St. Louis

Joe C. Pioletti handles individual and commercial bankruptcy, personal injury, wrongful death, workers’ compensation, and criminal defense at Pioletti Pioletti & Nichols. He earned his J.D. from SIU School of Law in 2013, holds membership in the Illinois State Bar Association, and is admitted to the U.S. District Court for the Central, Northern, and Southern Districts of Illinois and the Northern and Southern Districts of Indiana.

The firm has been a bankruptcy lawyer in St. Louis, MO for over 80 years. Because bankruptcy is federal law, the substantive rules governing Chapter 13 apply the same way everywhere. What changes from one district to the next is how the local court operates, what the Chapter 13 trustee expects to see in a plan, and how aggressively creditors contest confirmation. Our experience filing for Chapter 13 in the Eastern District of Missouri means we know where the practical pressure points are and how to prepare a petition that accounts for them.

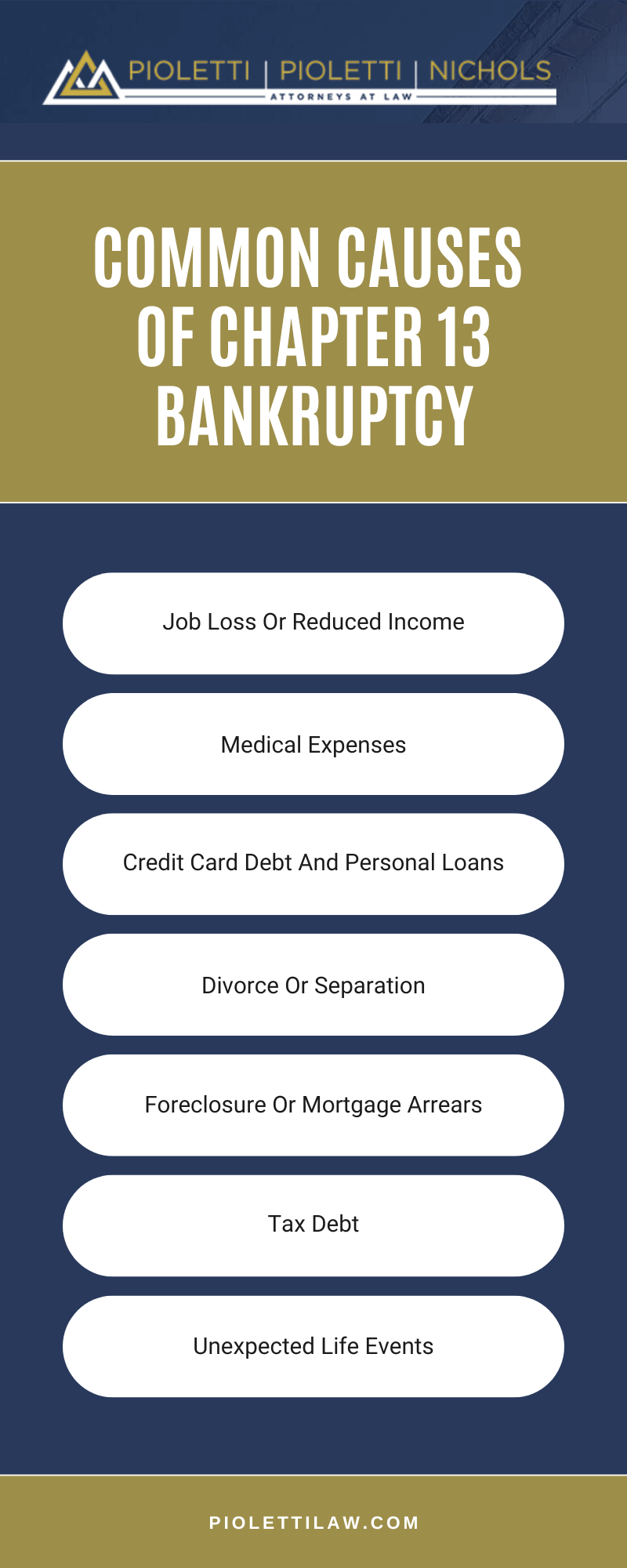

St. Louis Chapter 13 Bankruptcy Infographic

Understanding Chapter 13 Bankruptcy Cases

Chapter 7 vs. Chapter 13 and What Qualifies

Choosing between Chapter 7 and Chapter 13 is not a matter of preference. It depends on what you earn, what you own, and what you are trying to protect.

Chapter 13 requires regular income. You have to earn enough to cover your household expenses and still make a monthly payment to creditors through the plan. Chapter 7 does not require income; it is means-tested, and filers whose income is too high are pushed toward Chapter 13 instead.

The asset question is where the distinction matters most for St. Louis homeowners. Chapter 7 may require surrendering non-exempt property. Chapter 13 lets you keep everything, including a house in foreclosure or a car the lender is threatening to repossess. In exchange for retaining your property, you commit to a court-supervised repayment plan lasting three to five years.

There are debt limits on Chapter 13. They are adjusted periodically. If total debts exceed those limits, Chapter 11 may be the only reorganization option. The plan length depends on where the debtor’s income falls relative to the Missouri state median. According to the U.S. Courts, filers below the median generally qualify for a three-year plan; those above it typically must propose five years.

Chapter 13 also discharges certain debts that Chapter 7 does not, including some obligations from property settlements in divorce. The FTC debt guidance program outlines bankruptcy and non-bankruptcy options for consumers managing unaffordable debt.

Important Aspects of Chapter 13 Bankruptcy Cases

Three elements control whether a Chapter 13 case in St. Louis reaches discharge. The automatic stay, plan feasibility, and the Chapter 13 trustee.

The automatic stay kicks in the instant the petition hits the court. Foreclosures, repossessions, wage garnishments, and creditor lawsuits all come to a halt the moment that petition is filed. For a debtor in St. Louis who is two months behind on the mortgage or watching a quarter of each paycheck vanish to a garnishment order, the stay is the most immediate form of relief bankruptcy provides.

Plan feasibility is the hurdle that determines whether the court approves the repayment proposal. The monthly payment has to be realistic. If the budget the debtor presents does not leave enough room to fund the plan after covering rent, utilities, food, and transportation, the court will reject it. And falling behind on payments after the plan is confirmed can result in dismissal or conversion to Chapter 7.

The Chapter 13 trustee assigned to the case reviews the petition, examines the plan, and distributes payments once the plan is confirmed. The U.S. Trustee Program oversees bankruptcy administration in the Eastern District of Missouri.

Chapter 13 Bankruptcy Case Timelines

The timeline for a Chapter 13 case in St. Louis runs from the pre-filing requirements through the discharge, and the total duration depends on whether the debtor’s plan is three years or five.

- Credit counseling. Every Chapter 13 filer must complete a credit counseling course through an approved provider before the petition can be submitted. The certificate from that course is filed along with the petition.

- Filing the petition. The petition, financial schedules, and proposed plan go to the U.S. Bankruptcy Court for the Eastern District of Missouri. The automatic stay activates at that point.

- 341 meeting of creditors. Roughly 30 to 45 days later, the debtor sits for a meeting where the trustee and any objecting creditors can ask questions about the debtor’s income, expenses, and assets.

- Plan confirmation. A hearing follows where the court decides whether the plan satisfies the Bankruptcy Code. Creditor objections and trustee recommendations are addressed here.

- Payments and discharge. Monthly payments go to the trustee for the life of the plan. Once the final payment is made and the debtor completes a financial management course, the court enters a discharge order.

What to Bring to Your Chapter 13 Bankruptcy Consultation

We need to understand the full financial picture before we can advise on whether Chapter 13 is the right filing and how to structure the plan.

- Pay stubs or other proof of income going back at least six months

- The two most recent federal tax returns

- A complete list of debts, including creditor names, balances, account numbers, and whether each obligation is secured or unsecured

- Records for all assets, including the home, any vehicles, bank accounts, retirement savings, and anything else of value

- Copies of any creditor correspondence, court filings, garnishment orders, or foreclosure notices

We go through this material during the consultation, give you a direct assessment of whether Chapter 13 is the appropriate path, and explain what the monthly plan payment would look like based on your specific income and debts.

Missouri Legal Resources for Chapter 13 Bankruptcy Cases

Bankruptcy operates under federal law, but cases filed in St. Louis follow the local rules of the Eastern District of Missouri. The resources below provide background.

- The U.S. Courts bankruptcy website covers the bankruptcy process, including eligibility and procedural rules for each chapter.

- The U.S. Courts Chapter 13 page explains how Chapter 13 cases work from petition to discharge.

All St. Louis Chapter 13 filings are administered through the U.S. Bankruptcy Court for the Eastern District of Missouri.

Reach Out to Pioletti Pioletti & Nichols to Schedule a Consultation

If you are considering Chapter 13 bankruptcy in St. Louis, MO, Pioletti Pioletti & Nichols can review your financial situation and explain whether a repayment plan fits your circumstances. We have handled bankruptcy cases for over 80 years. Contact us to schedule a consultation with our St. Louis Chapter 13 bankruptcy attorneys.

Client Reviews

We are Members of