Trusted bankruptcy lawyers serving clients across St. Louis for over 80 years.

If you are struggling with debt in St. Louis and the collection calls have turned into lawsuits, garnishment orders, or a notice of foreclosure, bankruptcy may be the legal tool that gives you a structured way forward. The decision to file for bankruptcy involves careful consideration of the financial circumstances and the legal options available. It involves federal court, detailed financial disclosures, and rules that change depending on whether the case is filed under Chapter 7, Chapter 13, or Chapter 11. Pioletti Pioletti & Nichols has handled bankruptcy matters for individuals and businesses for over 80 years. Our St. Louis, MO bankruptcy lawyer can assess your financial situation and explain which path makes sense.

Bankruptcy Lawyer St. Louis, MO

Bankruptcy exists so that people and businesses drowning in debt have a legal mechanism to either eliminate what they owe or reorganize it into something manageable. The process runs through federal court, not state court. In St. Louis, that means the U.S. Bankruptcy Court for the Eastern District of Missouri. Which chapter applies, what debts can be addressed, and what happens to the debtor’s property all depend on the specifics of the financial situation.

Most individuals in St. Louis who file bankruptcy choose between two options. Chapter 7 wipes out qualifying unsecured debts through a liquidation process that wraps up in a few months. Chapter 13 sets up a court-supervised repayment plan that runs three to five years. The eligibility rules are different for each, and the consequences are different too. A St. Louis bankruptcy attorney can look at the income, the debts, and the assets and provide a clear recommendation on which chapter fits.

Types of Bankruptcy and Debt Relief Cases We Handle in St. Louis

Debt problems do not arrive in a single form. The homeowner who fell behind on mortgage payments after a medical crisis is in a different position than the wage earner watching a quarter of every paycheck disappear to a garnishment. Pioletti Pioletti & Nichols handles the following bankruptcy and debt relief matters in St. Louis.

- Chapter 7 bankruptcy. This is the liquidation chapter. Most unsecured debts are eliminated, and the case typically closes within three to four months. Filers must pass the means test, and Missouri’s exemption laws determine which property is protected from liquidation.

- Chapter 13 bankruptcy. Chapter 13 is built for people with regular income who want to keep their property while repaying debts over three to five years. One monthly payment goes to the trustee, who distributes it to creditors according to the plan. This chapter is often the right choice for homeowners behind on the mortgage or for filers whose income exceeds the Chapter 7 threshold.

- Chapter 11 bankruptcy. Primarily a business reorganization tool, though individuals whose debts exceed the Chapter 13 limits can file here as well. The debtor continues operating while restructuring financial obligations under court oversight.

- Car repossession. The automatic stay can halt a repossession before it happens. Under Chapter 13, the vehicle loan folds into the repayment plan, and in some circumstances the secured portion of the debt can be reduced to the car’s actual value.

- Debt consolidation. Chapter 13 functions as court-supervised consolidation. One payment per month to the trustee replaces the multiple creditor payments, different due dates, and collection pressure that come with managing unaffordable debt on your own.

- Foreclosure. Filing triggers the automatic stay, which stops a foreclosure immediately. Chapter 13 then allows the homeowner to catch up on missed payments through the plan while staying in the home.

- Wage garnishment. Bankruptcy stops garnishments the moment the petition is filed. The debt that triggered the garnishment is addressed through the case itself rather than through involuntary paycheck deductions.

- Means test analysis. The means test controls access to Chapter 7. It compares household income to the Missouri state median and factors in allowable deductions. We prepare clients for bankruptcy by running these numbers before the petition goes to court.

Why Choose Pioletti Pioletti & Nichols as My Bankruptcy Lawyer in St. Louis, MO?

Bankruptcy Representation in the St. Louis Area

Joe C. Pioletti is a member of the Illinois State Bar Association and handles individual and commercial bankruptcy, personal injury, wrongful death, workers’ compensation, and criminal defense at Pioletti Pioletti & Nichols. Joe graduated from Eureka College in 2010, earned his J.D. from SIU School of Law three years later, and holds admission to the U.S. District Court for the Central, Northern, and Southern Districts of Illinois and the Northern and Southern Districts of Indiana.

The firm has represented bankruptcy clients in St. Louis for over 80 years. Because bankruptcy is federal law, the substantive rules are the same everywhere. What changes from one district to the next is how the court operates, what the assigned trustee expects to see in a petition, and how aggressively local creditors contest filings. Our familiarity with the Eastern District of Missouri shapes how we draft petitions, build repayment plans, and prepare for objections that might otherwise catch a debtor off guard.

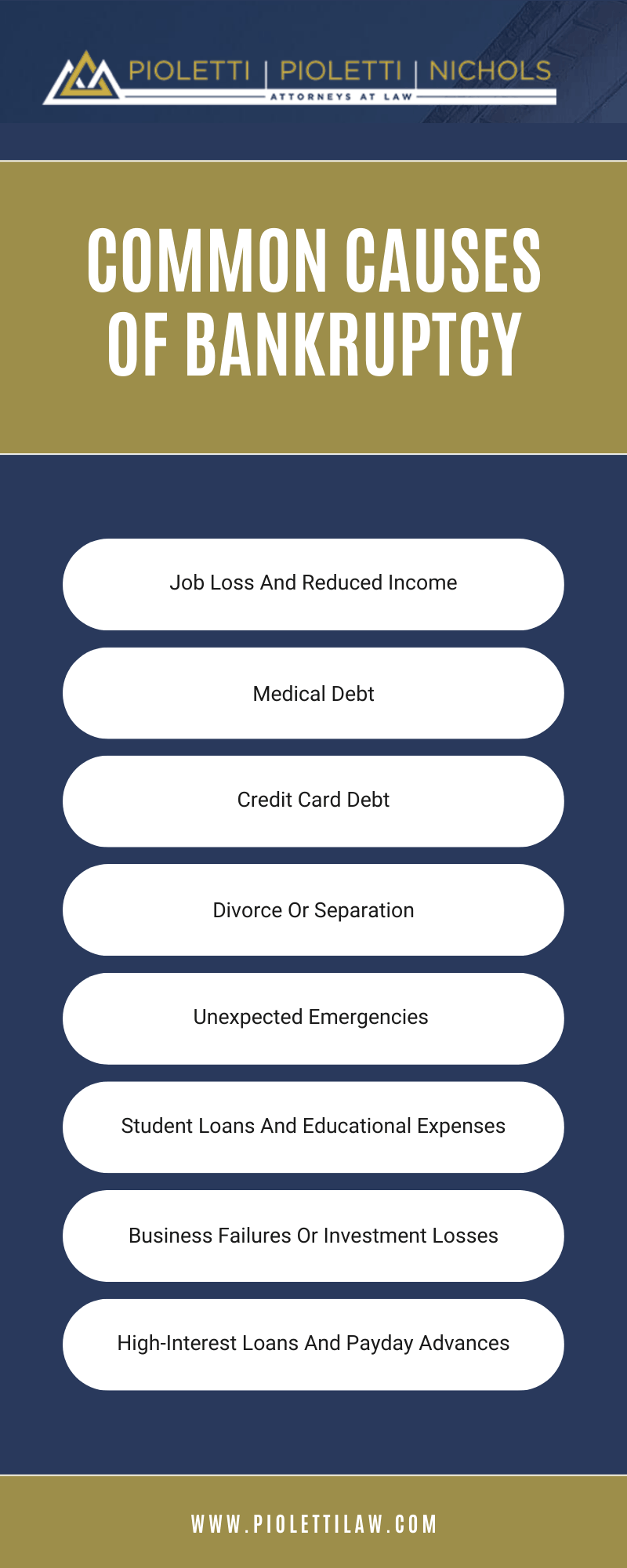

St. Louis Bankruptcy Infographic

Understanding Bankruptcy Cases

Chapter 7 vs. Chapter 13 and What Qualifies

Choosing between Chapter 7 and Chapter 13 depends on income, assets, and what the debtor is trying to accomplish.

Chapter 7 is liquidation. Most unsecured debts are eliminated, and the case moves quickly. But non-exempt property can be sold to pay creditors, and a debtor whose household income exceeds the Missouri median will not pass the means test. Chapter 7 works well when the debtor has limited assets and an income level that falls within the eligibility range.

Chapter 13 is reorganization. The debtor proposes a repayment plan covering three to five years, and according to the U.S. Courts bankruptcy website, filers whose income falls below the state median generally qualify for a three-year plan while those above it typically propose five. The advantage of Chapter 13 is that the debtor keeps everything, including a house the bank is trying to foreclose on or a vehicle that is about to be repossessed.

Certain debts cannot be discharged under either chapter. Student loans, most tax debts, child support, and obligations arising from fraud survive bankruptcy regardless of which chapter is filed. We assess which debts a filing will actually resolve before recommending a course of action.

The FTC debt guidance program outlines bankruptcy and non-bankruptcy alternatives for consumers dealing with unmanageable debt.

Important Aspects of Bankruptcy Cases

Three elements drive the outcome of a bankruptcy case in St. Louis, and each one requires attention from the beginning.

The automatic stay activates the instant the petition reaches the court. Foreclosures, repossessions, garnishments, collection calls, and creditor lawsuits all stop. For a debtor in St. Louis who is dealing with collection pressure from multiple directions at once, the stay is the most tangible form of relief bankruptcy provides, and it takes effect before the court has reviewed anything beyond the petition itself.

Protecting assets in bankruptcy is the second major concern. Missouri’s exemption laws determine which property a debtor can keep when filing under Chapter 7. A home, a car, retirement savings, and personal property are all subject to exemption analysis, and understanding how the state’s exemptions apply to a particular debtor’s situation is critical to avoiding unnecessary loss of property.

The trustee is the third element. The U.S. Trustee Program oversees bankruptcy administration in the Eastern District of Missouri. The trustee reviews the petition, examines financial disclosures, and in Chapter 7 cases identifies any non-exempt assets available for creditor distribution. How well the petition is prepared directly affects how that review goes.

Bankruptcy Case Timelines

The length of a bankruptcy case in St. Louis depends on the chapter. Chapter 7 cases typically conclude in four to six months. Chapter 13 cases run three to five years. The procedural steps, however, follow a consistent sequence.

- Credit counseling. Federal law requires completion of a credit counseling course before the petition can be filed. There are no exceptions.

- Filing the petition. The petition, schedules, and supporting documents go to the U.S. Bankruptcy Court for the Eastern District of Missouri. The automatic stay takes effect at that point.

- 341 meeting of creditors. Roughly 30 to 45 days after filing, the debtor appears for a meeting where the trustee asks questions about the financial disclosures. Creditors may attend but rarely do in straightforward cases.

- Discharge or plan completion. Chapter 7 discharges typically arrive within 60 to 90 days after the 341 meeting. In Chapter 13, the debtor makes monthly payments for the duration of the plan, and the discharge follows the final payment and a required financial management course.

Rebuilding credit after bankruptcy takes time and discipline, but many people who have been through the process qualify for new credit within one to two years of the discharge.

What to Bring to Your Bankruptcy Consultation

The first meeting is about numbers. We need a full picture of income, debts, and assets before we can recommend a chapter or begin drafting the petition.

- Pay stubs or other proof of income going back at least six months

- The two most recent federal tax returns

- A complete list of debts with creditor names, account numbers, and balances, noting which are secured and which are unsecured

- Records for all assets, including property, vehicles, bank accounts, retirement funds, and anything else of significant value

- Any correspondence from creditors, collection agencies, or courts about pending lawsuits, garnishments, or foreclosure proceedings

We go through everything during the consultation, assess which chapter applies, and explain what the bankruptcy process involves from that point forward.

Missouri Legal Resources for Bankruptcy Cases?

Bankruptcy operates under federal law, but cases filed in St. Louis follow the local rules of the Eastern District of Missouri. The resources below provide background.

- The U.S. Courts bankruptcy website covers the bankruptcy process, including eligibility and procedural rules for each chapter.

- The U.S. Courts Chapter 13 page explains how repayment plans work from petition to discharge.

All St. Louis bankruptcy filings are administered through the U.S. Bankruptcy Court for the Eastern District of Missouri.

Reach Out to Pioletti Pioletti & Nichols to Schedule a Consultation

If you are considering bankruptcy in St. Louis, MO, Pioletti Pioletti & Nichols can review your financial situation and explain the available options. We have handled bankruptcy cases for over 80 years. Contact us to schedule a consultation with our St. Louis bankruptcy attorneys.

Client Reviews

We are Members of